Over the past couple of weeks I have been lobbying as many members of the House of Lords as I can with the following email as they debate the EU (Withdrawal) Bill. This is not an easy task as there are restrictions on bulk emails, but thankfully many members retain their own personal addresses, and there are ways round the central system to some extent anyway. So here is what I have sent.

Dear Lord or Baroness X

THE ECONOMIC CASE FOR BREXIT

I should be grateful if you would spare a few moments of your time checking out the economic case for Brexit which I set out below. This has scarcely been examined in any detail in public and we face the terrifying prospect of members of both Houses taking momentous decisions about the future of our country without the benefit of a full and proper briefing. There is no need to depend on the type of bland assertions, lazy assumptions, dodgy forecasts and personal opinions with which the establishment has bombarded us. Hard facts and logic are available and compelling.

Do we really want to carry on like this?

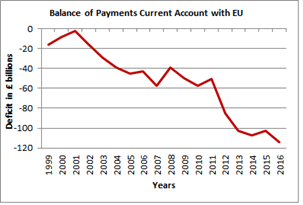

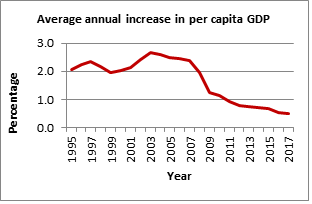

I start with a couple of graphs using data I have downloaded from the Office for National Statistics’ website.

The first shows a deterioration in our trade deficit by almost 6% of GDP over the past twenty years, whilst the second shows how average incomes are growing at an ever slower and paltry rate. With widening income and regional gaps it is likely that many people are experiencing a real fall in their standard of living. This coincides with the onset of globalisation and our joining the EU Single Market. The EU been responsible for our trading affairs over this period of time and is thus guilty of monumental failure. That alone should be sufficient to sack them.

The link between trade and economic growth

I am not talking here about the correlation between global growth and free trade, which is well supported by research. A closer look at that research however shows that it is only the surplus countries, like Germany, Japan and China, which benefit, while deficit countries like the UK and US have missed out and declined. There has in fact been a transfer of existing wealth from the deficit countries to the surplus countries as well as growth in the recipient ones.

At national level a deficit is like having a hole in the bottom of our economy. If nothing were done about it unemployment would go through the roof. Fortunately the Bank of England has been able to put its finger in the dyke using Quantitative Easing. This works by reducing interest rates thereby encouraging people to borrow more, save less and use up their existing savings. As Mervyn King put it in his recent book, The End of Alchemy, people are now spending their future earnings today. This, he goes on, cannot continue for long because sooner or later tomorrow becomes today and they cannot borrow any more. They will also have used up existing savings. The low interest rates also have the effect of limiting saving, which starves the banks of money to lend to business for investment in new technology and productivity growth. The productivity gap has been well documented as you know, though curiously the obvious cause ignored. This does lead me to suppose that the establishment is only showing us the side of the coin it wants us to see.

It is therefore imperative that we end QE to increase interest rates by balancing our trade before a new financial crisis hits us and to re-establish savings and growth. There are only two ways this can be achieved; though devaluation and by increasing our import tariffs. We have already had some benefit from devaluation following the referendum, but its size is determined by the markets. That just leaves import tariffs as a direct instrument of government.

Whilst a no-deal Brexit will be a substantial step in the right direction, there is no guarantee it will be enough. We must retain the flexibility after Brexit to set our import tariffs at a level which will balance our trade. This may mean delaying re-joining the WTO. Conversely any attempt to do a trade deal with the EU, or anyone else for that matter, will limit that flexibility, whilst remaining in the Single Market will lock us into the £115bn trade deficit we currently have. We would then be completely stymied and helpless. Please note that the Government’s enthusiasm about the opportunities for doing trade deals around the world is misplaced, at least until we have established a balance. Indeed this is also the principal reason why the Doha round of global trade talks collapsed; the precondition of balance was not met.

Jobs

We all want to see the creation of more jobs, particularly in the manufacturing sector outside London and the South East, and I am not surprised the Labour Party have recently made this their priority. Their tragedy is that they have got the argument completely back-to-front, by concluding it requires us to remain in the EU customs union and single market when the very reverse is the case.

Even though the above graphs show clearly what a disaster EU membership has been for trade and growth in the UK, the following logic demonstrates it further. We have this massive trade deficit with the EU. That means our imports are greater than our exports. Suppose now we place import tariffs on both sides of the channel, which is what a no-deal Brexit would involve. The result will obviously be a reduction in the volume of trade. Assuming the tariffs are at the same percentage level on both sides, the reduction in percentage trade volumes will be similar. But that means that the absolute reduction in imports will be greater than the absolute reduction in exports since we start with a deficit. This in turn means that the number of new jobs created from import substitution will be greater than the number lost to export substitution, ie a net increase. In short it is the balance of trade that matters, not the volume.

Inward Investment

One of the more amusing spectacles in recent weeks has been that of the Japanese ambassador claiming that Brexit would discourage investment into this country. Now that really is trying to have your cake and eat it! UK manufacturers have already had a competitive boost of about 12% from devaluation, so the 10% cost of EU vehicle import tariffs will still leave them better off. The two go together.

There has also been much talk about supply chains. These will chop and change as a matter of course anyway, but any disruption could be minimised by not charging tariffs on components and spare parts. This would have the added advantage of encouraging all vehicle manufacturers to do their final assembly here in the UK.

The Brexit Fiscal Dividend

Much has already been written about the savings from EU budget payments and I don’t propose to go over old ground here. I trust it is fair to say that a net saving of £10bn a year is not controversial. It is other savings that have been overlooked.

First there is the matter of import tariff revenues on imports from outside the EU. These amount to about 60% of all imports of some £625bn a year, on which the EU customs union currently collects just over 4% as import tariffs, ie about £15bn. We pay 80% of these, £12bn, over to Brussels. Clearly after Brexit we will continue to collect this money. Nor will it cause any inflation to do so as it is already in force. All that will change is that we will keep the £12bn for ourselves! Funny how nobody ever mentions that. So that now gives a total dividend of £22bn.

But that is not all. We will of course also start to collect tariffs on our imports from the EU, another £10bn, total now £32bn. There will be some price increases from this, but spread over the whole economy they will contribute only about half a percent to inflation on a once off basis. Big deal.

There is more. A few months ago the Bruges Group produced a paper calculating savings from welfare and pension payments to immigrants and non-residents in the order of £35bn. You can find it at http://www.brugesgroup.com/blog/brexit-the-end-to-austerity. I have not been able to verify these figures myself, so to be safe let’s just accrue half, £18bn. That gives a total annual Brexit dividend of £50bn a year, FIVE TIMES the number that was bandied about during the referendum campaign.

How could any government in its right mind even think of throwing this sort of money away for nothing? Yet that is precisely what the Remainian camp are proposing to do. We need that money.

The Economic and Political cycles

Do not be lulled by the latest indications of a fiscal surplus. This is just a cyclical anomaly caused by the combination of loose monetary policy and tight fiscal policy. Neither is sustainable, the former economically as I have explained above, and the latter politically. Before long politically irresistible calls for tax cuts from the Right and/or expenditure increases from the Left will destroy the balance just as the former did in the late 1980s resulting in the boom and bust. Let us not repeat the same mistake.

Brexit offers us a way out by enabling us to tighten monetary policy to increase interest rates as the trade deficit is reduced, at the same time as loosening fiscal policy using the Brexit dividend to assuage political pressures, thereby keeping the two in balance. Carpe diem.

Your support

The European Union (Withdrawal) Bill after completing the House of Commons is now progressing through the House of Lords. Your support for this will be greatly appreciated by millions of voters including myself. Whilst most voters will not understand the economic technicalities I have described above, they most certainly feel the results, and they are angry. The problem is exacerbated by the widening income and regional gaps so that Remainers on their massive metropolitan salaries are insulated from the consequences and do not feel them. This is not some right-wing xenophobic populist aberration; this is genuine democracy in action and a recipe for conflict if ignored and which will only increase without a no-deal Brexit.

I ask you to conclude the European Union (Withdrawal) Bill’s passage through the House of Lords without opposing it or seeking to water down Brexit. And above all else without stipulating that there should be a further and thoroughly unnecessary second referendum. Nor should there be an opportunity for the decision to leave to be overturned. As a democrat I earnestly hope that in accordance with the referendum, the general election, and the EU (Notification of Withdrawal) Act, you will also approve the European Union (Withdrawal) Bill.

Please keep faith with the electorate and help restore our economy.

Yours sincerely,

John Poynton FCA

16th March 2018