I started to think so last weekend as I read his column in the Sunday Telegraph business section. Each week Warner provides a Remainer view while on the same page Liam Halligan gives a Leave perspective. I always read both as I enjoy the challenge of debunking Warner’s arguments, but this week I found him saying some things which are undoubtedly correct.

First he acknowledged that we have a massive and increasing current account (trade) deficit. He also saw that this is being funded, in foreign currency, by massive capital inflows, causing an increase in the value of the pound making it less competitive. He noted the devaluation since the referendum and the consequent small reversal in the deficit, but was inclined to attribute the reduction in the deficit more to the buoyant international economy than to devaluation. He then observed that many manufacturers had scaled back investment since the referendum, and even acknowledged this may simply due to uncertainty and concluded by admitting to a degree of uncertainty himself. None-the-less, he stuck to his Remainian position!

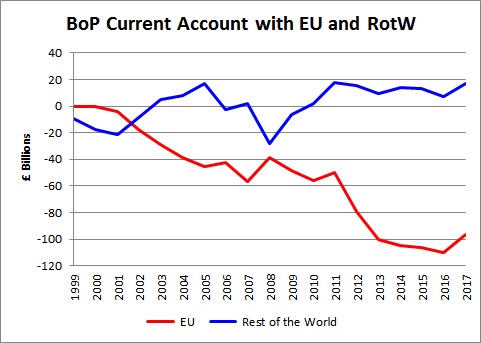

What he failed to point out of course was that all and more of our current account deficit is entirely and solely due to our trade with the other EU countries, as shown in this graph. Our trade with the Rest of the World is actually in surplus. So why the divergence?

He is probably right to observe that our exchange rate is not hugely over-valued, otherwise why would our trade outside the EU be so successful? Nor can it due to tariffs as there aren’t any within the Single Market. He also failed to point out that under-investment and the consequent ‘productivity gap’ goes back to the banking crisis and the start of QE, rather than just to the referendum.

I covered this point in my recent facebook post in response to an IEA podcast, and concluded that the only possible cause of the EU deficit is that over the past twenty years Brussels has methodically and surreptitiously been piling up a great stack of regulations and other non-tariff barriers against us. Whether this has been by design or by accident I leave you to ponder! Either way it means that we must recover control over our terms of trade if we are to have any chance of reversing the deficit and thereby avoiding a massive recession when people can’t borrow any more. That is only possible through a No-Deal (WTO terms) Brexit. Any sort of deal with the EU will lock us into this disastrous trend. Even so, it will take many years of painstaking work to unravel these non-tariff barriers. In the meantime tariffs on both sides of the Channel will help to reduce the deficit and create jobs as people revert to buying British rather than foreign, and the Treasury will have a further £25bn or so of import tariff revenues to help with the fiscal position. Exports are likely still to thrive as devaluation at around 12% is far greater than the average tariffs we will face. We would also have the money to subsidise any exports facing tariffs in excess of 10% if we wish. See also my facebook page for a description of how the max-fac import system could work – it does not require any software investment by industry at all!

It is the re-starting of QE together with consequent record levels of personal debt which gives the game away. The Treasury don’t want you to know this as they were facing a big problem in financing the trade deficit domestically before the referendum. They were under pressure to increase interest rates and restart savings and growth. It is not just about paying import bills in foreign currency; it is also the fact that if both we and foreigners are buying more foreign stuff instead of British then unemployment will rise.

If it really is the case, which traditionalists will argue, that the capital inflows will convert into job-creating investment by industry then why restart QE? The reality is that most of those inflows are simply going into the property market and inflating other assets.

So the Treasury were delighted when they could blame the referendum for the restart of QE, when in reality it had nothing to do with the referendum and everything to do with financing our EU trade deficit. They could even wave their arms about and point to a reduction in unemployment and record job numbers when in fact all they had done was puff up the economy using QE. But in truth it is a con as such a policy is unsustainable. Who will be around when these chickens come home to roost?

Finally a comment on the position of the other parties. Labour, entirely in keeping with their historic and somewhat tenuous relationship with the science of economics, say, as we do, that they want to protect jobs; and then get the technical argument completely back-to-front! It is the No-Deal Brexit which will create and protect jobs, not any deal with the EU as they favour. Neither should we fall into the arms of Jacob Rees-Mogg, who looks forward to eliminating import tariffs on food, clothing and shoes. This is Jacob’s very own magic money tree! Yes of course we would all like lower import prices, but as everyone then buys more foreign than British unemployment will rise. It is the balance of trade that matters, not the volume or the level of import tariffs.

As with the ERM and the Euro, once again only UKIP gets it right!