So, Labour wants to freeze rail fares. All very popular of course, but no indication as to how they would actually fund that. Would they really be so grossly irresponsible and incompetent as to just load that onto general taxation and create more fiscal black holes? Past experience suggests so. But if our railways are not adequately funded they will go bust and the whole network would go down. We cannot let that happen. They are a monopoly and that requires a new approach to funding which protects both the consumer and the taxpayer from profiteering, including the cutting of operational costs that undermine quality of service. Most of us remember the underspending on maintenance that followed the Conservative attempt to privatise the railways in the late 90’s and the horrendous crashes that ensued. That was a failure of regulation. Not the way to do it.

There is in fact a strong case for subsidising rail fares. We want to ensure that the massive investment we have already made and may yet make into this infrastructure is used to optimal extent, and we want to minimise congestion on our roads. That would suggest some sort of cross subsidy between the two with road users picking up the tab. After all not all of us use these services. Why should those who don’t have to subsidise those who do?

Indeed there is also a strong case for ring-fencing the whole of the transport budget. It is just about the only departmental budget that does not necessarily involve any transfer of wealth from rich to poor. Revenues from transport fuel duties and other charges currently amount to c.£24bn whereas departmental expenditure is only £14bn. If the whole of the revenues were given over to that Department and kept quite separate from the Treasury then users and only users would get the full benefit from them including any cross funding and subsidy for the railways. Decisions over road pricing for example could also be left to that department which would become entirely self-funding perhaps through a new National Transport Corporation.

To nationalise or not to nationalise? Is that the question? NO! Absolutely not! If you nationalise a capital intensive industry such as our railways all the capital costs of modernisation and expansion, tens of billions of pounds’ worth (look at HS2) will fall onto the shoulders of the taxpayer. Most of us want to see taxation below 30% GDP in the belief that will enhance economic growth, which is not an unreasonable target given it was 33% (plus fiscal deficit) before Covid. Now it is around 38% with a massive 6% GDP deficit on top. The taxpayer simply cannot afford that sort of expenditure. It has to come from the City.

But to attract funding from the city requires profits. One thing I have noticed over the years is just how risk averse institutional investors can be. Safety and guarantees against loss are just as if not more important to them that exceptional profits. This would suggest cap and collar profit regulation with a collar at say 2.5% profit before tax and a cap at 7.5%. Or maybe lower if experience shows funding can be raised without underwriting at these levels. If profits come out above the cap the regulator would require fare cuts to bring profits back to the centre of the range, other things being equal , and HMRC would claw back the excess profits.. That still leaves shareholders with an incentive to rebuild profits back up to the cap through greater efficiency. However if profits fall below the collar the regulator will allow corresponding increases or, line by line or service by service, closure if fare increases reduce turnover still further. HMRC could refund profit shortfalls, charging the amount to the Department of Transport.

Reintegration of the railways does not imply nationalisation. Splitting the service up into lots of local operators has just created lots of little monopolies, and in any case the franchise system was always going to be inappropriate to such a capital intensive industry which requires large long-term capital investment. Franchising is fine if you running chain of burger bars, but not here. That said I have no objection to private operators buying in perpetuity rights to slots in a national timetable set by Network Rail with a secondary market allowing them to be bought and sold. A substantial service charge from Network Rail (subject to regulation) would ensure they are only kept if they can be made profitable, and that would allow new operators to enter the market where existing supply is insufficient or inefficient. The fact that this has not happened much in practice is again a failure of both organisation and regulation which focuses on comparisons with general inflation rather than profitability.

But we are still left with three problems:

1. How to fund and allocate subsidies to ensure an optimal balance between, and utilisation of, road and rail services.

2. How to set fares locally so they reflect local levels of demand, and

3. How to allocate capital expenditure to where demand is greatest.

It is important that any subsidy system promotes incentives to maximise turnover. Turnover is maximised by satisfying the right combination of consumer demand on price, availability and quality of service. Only the price mechanism, driven by the purchase decision, can provide this. Look at the NHS by comparison. Generally high on quality of service, but hopeless on both availability and efficiency, and the same is true of all other public services.

I therefore recommend a general and uniform turnover percentage uplift subsidy across the industry to replace all other forms of subsidy, but leaving open the option for local authorities and others to add their own percentages for local services if they wish. It should also replace the train drivers wage subsidy, (but I digress!). Indeed, to digress further, any losses such as passenger refunds and other losses directly attributable to strike action should be recharged to the Unions. A good employer does not underpay his staff. If you do you will lose them and the best will go first. In the private sector we judge this by looking at staff turnover rates and recruitment response rates, and the public sector should do the same. This is not something that can be done through national wage bargaining. It has to be done locally because the ‘rate for the job’ will vary across different skills, in different locations and at different levels of experience. The same is true in setting rail fares. Thus some services will produce profits in excess of the cap and other losses below it. The regulator would only alter the national subsidy level if total profits fell outside the limits, but may require fare reductions on specific services. The national subsidy would be set so that a small number of services do close each year.

The Regulator must also take an interest in whether sufficient expenditure is being spent on maintenance and safety, and approve capital expenditure plans to ensure they reflect local patterns of actual consumer demand and well as safety requirements. Network Rail would issue just enough new shares each year to fund approved capital expenditure programmes so we would see a gradual re-privatisation over a number of years rather than the dramatic ‘Tell Sid’ exercises favoured by Margaret Thatcher which invariably undersold taxpayer assets.

Indeed the Cap and Collar Profit Regulation model should be rolled out for all our monopoly utilities. The Water industry is another pressing example. And essential multi-supplier services such as farming and care homes would also benefit from the national turnover subsidy with cap and collar profit regulation model but with no need for price regulation because there is sufficient competition.

But don’t hold your breath. Do I see these ideas in any of the party manifestos? No I don’t. They all seem more interested in campaigning than policy.

Most people are familiar with the Peter Principle which states that in most organisations people are promoted to one level beyond the limits of their competance. This explains why so much senior management is incompetent.

However the same thing surely applies to family size. Most families have one or more children more than they can afford. It does’t matter how rich they are (within reason) or how many benefits they receive, they will always dilute their average earnings per child to below the definition of child poverty – using the official definition which is a percentage of average earnings rather thah any assessment of actual serious deprivation. This definition also produces the perverse result that child povery declines during a recession and vice versa.

I had an interseting exchange of emails with the late Cheryl Gillan some years ago in which she sent me some statistics showing that on average families on benefits have more children than those not on benefits. I have always wondered whether this correspondance was influential in the decision shortly afterwards to introduce the two chlld cap to child tax credits.

It follows that any decision by Labour to scrap the cap will do nothing to reduce child poverty. Instead we should scrap child tax credits altogether. It is an anomolous system introduced by Gordon Brown administered by the Treasury when he fell out with Frank Field at the the DWP and is incompatible with it. It has different claw back rates and earnings disregards so that in some circumstances appling for the one you can lose more from the other! Coming at a time when we must do everything we can to incentivuse people back into work, it is perverse.

It would be a simple matter to add one child tax credit to every adult universal credit and scrap them. This would result in no change in benefit income for 2 parent 2 child families, or 1 of each, and existing larger families could stay on the old system until they had grown out of it. But it would completely remove the incentive to breed for benefits and give a welcome one-off increase to single adults. The reduction in the birth rate would pay for the latter.

Mr. Speaker, it is an honour and a privilege for me to have this opportunity to present to the House the government’s budget for the coming year.

As the House will already know, our economy and government finances are in a desperate and sorry state. Over the past nearly 25 years we have suffered a series of setbacks that have enveloped us in a perfect storm, starting with our membership of the European Union Single Market which has seen our trade balance with those countries plummet from having been broadly in balance to a deficit at the time of the Brexit Referendum of £109 billion; that’s 6% of GDP at that time. This has presented British business with a contracting market. Generally speaking business will not invest into a contracting market, with the result that productivity growth has suffered.

Then we had the banking crisis, triggered by an oil price spike in 2007 which led to the default of many sub-prime mortgages in the USA and which our banks had invested into. But there were also collapses on this side of the pond such as Northern Rock and HBOS which were simply due to over-trading, and that can only be due to a failure of regulation here. One bright spot then arises as the banks were quickly recapitalised through the use of quantitative easing, which did not on that occasion produce inflation as it was merely replacing credit which had been destroyed in the crisis. Unfortunately later on the QE was restarted with inevitable inflationary consequences.

On top of all that we had austerity and the failure to start a Sovereign Wealth Fund when interest rates hit the floor. Mr. Speaker, I am sure that most members are aware that 5% compounded will quadruple your money within 30 years, and 7% double it within ten. Over the past thirty years returns on many foreign shares have been far greater than the cost of government borrowing here. That is because the rate of growth in many other countries has been far faster than it has been here and is likely to continue that way for some time to come. It must make sense for us to benefit from their success in this way. A golden opportunity completely missed.

Then we come to Brexit which some today are blaming for all our financial woes. Mr. Speaker, I do not accept that analysis but instead that the Trade and Co-operation Agreement has locked us into the catastrophic trade deficit we inherited from the Single Market. It is not enough to secure no tariffs in either direction when there are a host of other regulations creating the imbalance, and we need the use of tariffs to counter that effect. That will almost certainly mean scrapping the TCA, and whilst trade volumes may fall, the much greater effect of import substitution will present British business at home with the expanding market they crave to invest and create productivity growth and jobs.

Following that we had Covid and the energy crisis caused by the war in Ukraine, thankfully temporarily as Russia has found other outlets into the international oil markets, and all of the panic over climate change. And if that weren’t enough mass immigration, quite apart from increasing cultural conflict within the country, has condemned wages to minimum levels, undermined working conditions and caused record levels of unemployment and homelessness. And to cap it all, we have an ageing population pushing the cost of pensions and health care through the roof. Oh dear, oh dear, oh dear!

Now, Mr. Speaker, it is not my intention to spend time trying to apportion blame for this situation. Many of these circumstances were beyond our control, and for others it is easy to be wise after the event. My purpose is to identify the causes so we can take appropriate action to remedy them and to quantify the task itself. Our National Debt is now close to 100% of GDP after having been nearly paid off a quarter of a century ago, and the cost of interest on that debt is now over £100 billion a year, nearly 4% GDP in itself, and rising. The total fiscal deficit is around £170 billion and that is adding to the Debt all the time. It is imperative, Mr. Speaker, that we get our nose ahead of the game so that we can reverse the whole process.

My strategy is based on three key objectives necessary to provide a tripod of stability for our recovery. First I aim to achieve a fiscal surplus of 1% GDP within five years. Second I want a trade surplus of 1% GDP by that time, and third we must achieve net zero immigration as well. Add to that some essential tax cuts to motivate growth and expenditure increases to avoid imminent collapse of some public services and we are looking at an annual fiscal turnaround of £300 billion by the end of our first five years.

On average I must save £60 billion in each of the next five years, but that is only on average. There are couple of policies which can raise substantial funds in excess of this amount up front, while others such as revived economic growth will be weighted towards the end. The good news is that over the following five years those trends should lead to a much greater turnaround of around £450 billion or more, with much greater scope for both tax cuts and expenditure increases, which I shall aim broadly to keep equal. I shall also aim to cut the total level of taxation down to 30% GDP, whereas currently it is around 37%, all the while maintaining fiscal and trade surpluses of 1% GDP. History shows that all the economies with the highest rates of economic growth have run Balance of Payments surpluses and I am determined the UK should be in that group.

So, Mr. Speaker, let me make a start.

My first port of call is multinational corporations, which have long had a habit of shifting their profits into tax havens, or semi tax havens such as the Republic of Ireland, to avoid corporation tax in this country. Now I accept that at 25% our rate of corporation tax is too high, and I shall return to that later, but for now may I completely reject the argument that this country must somehow engage in a race to bottom just to remain competitive. There are other ways we can regulate our trade balance, and in any case if were able to collect what is morally due to us, profits made out purchases by the good citizens of this country, that would provide the funds to reduce it.

Over ten years ago now, the G8 at its summit in Enniskillen tasked the OECD with ending this practice. They have completely failed to do so and show no signs of any significant progress as they just kick the can further on down the road. Clearly the multinationals have got to them! We cannot afford to wait any longer.

The good news is that this is very easy to rectify. Henceforth multinationals, which we shall define as any company that has more than 10% of its turnover in more than one country, shall be taxed on the basis of their global profits, as declared to their shareholders and in the public domain, and apportioned to this country by turnover, including non-domestic intercompany sales. They may be able to shift their head offices and their intellectual property rights, but they cannot shift their customers! It is difficult to forecast accurately without an established database exactly how much additional revenue this will raise, but our best estimates suggest it could be within the range of £40 to 50 billion if not more.

Second, Mr. Speaker, I am abolishing Inheritance Tax. It is a very inefficient tax, raising only about a third of 1% GDP; is double taxation in the hands of the deceased; uses up a disproportionate amount of tax legislation and consequently distracts the attention of thousands of lawyers and accountants who should be more constructively engaged.

However I recognise that a society in which around 2% of the population own 80% of its assets is not a healthy one. I want to reduce this wealth gap but not eliminate it. It remains important that those with energy, ability and enterprise can profit from them for the benefit of us all. In practice however much of this accumulated wealth is passive asset appreciation.

I therefore aim to raise about 2% GDP by charging legacies to capital gains tax in the hands of beneficiaries. This would require a 50% withholding tax to counter avoidance, but which would be repaid, with interest, when the gains are presented for assessment. I do not propose to introduce a wealth tax, which would also be double taxation in the hands of the taxpayer as well as very difficult to collect as much of it would disappear into overseas trusts and corporate structures.

Capital gains will be assessed to income tax at the taxpayer’s marginal rate with no additional allowances. However I am allowing it to be spread over ten years so that poorer beneficiaries can use up more of their allowances and lower rate bands. This reflects the rule-of-thumb PE ratio of 10 often used to value small companies.

Existing roll-over reliefs from inheritance tax such as for farms and businesses will be maintained and I am adding relief for the repayment of any student loans, not necessarily those of the taxpayer. Tax on occupied primary residences, again not necessarily by the taxpayer or his family, such as a sitting tenant, may be deferred until that occupant leaves.

I am also abolishing Non-Dom status, but replacing it with a flat cap on income tax, including capital gains, of £250,000 in any one year.

These two changes alone should raise around £80 billion a year. I am not seeking to raise any other taxes. I am however reintroducing marginal relief from corporation tax for small businesses with a zero rate allowance of one million and a lower rate band of two million. The lower rate will be half the full rate which remains at 25%. In the longer term I aim to reduce taxation to 30% GDP and increase the personal tax allowance to match the typical minimum wage at £20,000, and reduce the top rate to 40%. I may also introduce an intermediate rate at 30%.

Mr. Speaker I now come to a series of changes focused on reducing the burden on the taxpayer without endangering essential public services by focusing on efficiency and alternative sources of finance.

Better late than never I am introducing a Sovereign Wealth Fund which will be funded by borrowing at an interest rate not greater than 5% and at an amount, if available in the gilts markets, of 1% GDP a year. The asset will offset the liability and therefore have no effect on net debt. This will be farmed out to multiple professional fund managers with after time the more successful attracting greater contributions.

In addition I am starting the funding of a new state pension. This necessarily must be a gradual and prolonged process which will not have any significant effect on the public finances for many years. It will be available only to those under the age of 25 on 6th April next year and will be optional. Modelling suggests it will primarily benefit those on above average salaries, thereby halving in due course the number in the existing state pension. This in turn may allow us to improve the existing state pension significantly. For those who opt in, the existing employee national insurance contribution of 8% becomes a national pension contribution and is placed in an account in their name to which a guaranteed 4% interest as added annually. Of the three parameters of contribution rate, retirement age and pension amount, they will have the flexibility to fix any two and get a quote for the third. They may opt in or change these parameters at a later date, subject to not reducing the pension to an annuity equivalent below the level that would trigger entitlement to pension credits, and their remaining entitlement to the existing state pension will be determined by the number of years’ contributions in the existing way. This will create a fully flexible and transferable pension scheme which is currently unavailable to many, including those who switch employment between the public and private sectors. The money will physically go into the Sovereign Wealth Fund, which should get a better return for carrying risk, and will be part of its 1% GDP per annum funding target.

Mr. Speaker I am also introducing a National Credit Card. The purpose of the card is to give all citizens access to the private sector for essential services such as health and education on a means-tested basis. Just taking the health and schools budgets alone costs the taxpayer around £250 billion a year. If 50% used the private sector instead, and the average means-tested support for fees was also 50%, then the saving to the taxpayer would be over £60 billion a year.

We shall have to introduce this gradually to enable the supply side to meet increasing demand and it will be optional. Users pay for services in the normal way but do not have to settle the card at the end of the month. Instead after the end of the year when the taxman assesses your tax he will also review how much you have spent on your card, put the two together and recharge your share of the cost to your tax bill for the following year. Working capital will come from the Sovereign Wealth Fund at 5% which will be added to your costs from the date of purchase, but users will be able to pay on account to avoid it. The means test rate will be a simple percentage set at the beginning of each fiscal year for each user set in due course to encourage 50% usage. Much of these savings will then be available to improve the state services, and the fact that the private sector is accessible to all will remove any stain of privilege that some attribute to it at present.

Mr. Speaker, with the help of my RH colleagues I am taking a number of measures to improve efficiency within our public services. First we shall be splitting the civil service clean in two so that the advisory side, which advises ministers on current problems and future legislation, becomes completely separate and independent from the executive side, which delivers services mandated by Parliament. Two completely separate functions requiring separate organisational structures. This way the advisory side can assist ministers in holding the executive side to account.

Second we shall be appointing a national chief executive with the power to hire and fire local chief executives for every national public service. It is an extraordinary fact that currently few if any of our public services actually have any top management at all. No wonder they are all running around like headless chickens being hopelessly inefficient.

These chief executives will be mandated to ensure that sufficient trained British staff are recruited into each service, that they are paid the rate for the job so that staff turnover rates are minimised, and that agency and support staff are reduced to less than 25% of payroll each.I am also allowing staff bonuses to be paid out of 10% of any local budget savings or collected charges.

Third, I am abolishing national wage bargaining in the tax funded public sector. Henceforth all such staff will be paid a full inflationary increase on 1st April each year. I reject the argument that this will create an inflationary wage spiral on the grounds both that there are no prices in this sector and that inflation increases the tax base anyway. But it is also important for staffing stability that all staff are paid the rate for the job, which will vary by skill and location across the country with additional increases awarded locally and which therefore cannot be addressed on a national basis.

These measures taken together could save another £30 billion a year as well as ensure they are no longer dependent on immigration for staff.

Speaking of immigration, my RH friend the Home Secretary will be scrapping the current points-based system and replacing it with an auctioned reducing quota system so that total immigration is reduced to below emigration rates within five years. It is therefore vital that we are able to reduce unemployment at the same or faster rate. Indeed we currently have over 3% job vacancies across our economy which is roughly double historical norms and only serves to suck in yet more immigrants. I shall therefore be instructing the Bank of England’s monetary policy committee henceforth to use a composite 4% target when setting interest rates; that is 2% inflation plus 2% job vacancies. I anticipate this will mean interest rates will remain at around the 5% mark for the foreseeable future, which is necessary anyway to encourage savings and fund investment, and will also probably be needed to contain the inflationary impact of wage rises in a tighter labour market. I shall be addressing the housing market separately in a few moments.

In addition I have a new regional policy designed to reduce the regional pay and unemployment gaps. It must make sense to focus stimulation to where unemployment is highest post code by post code across the country leading eventually to an even level of percentage employment across the land. This will increase income tax revenues and reduce welfare claims so it is likely to be fiscally neutral in the longer term.

To do so I shall cease funding new free tax and enterprise zones, which have a very chequered and uneven history, and instead introduce discounts for income tax, business rates and employers national insurance where the discount is proportionate to the local level of unemployment. For the coming year this discount will be 5% for every 1% that unemployment, measured on the claimant basis, is above 5%. We will review this algorithm annually to ensure a steady reduction in the regional gap.

I also have a number of measures to free up the labour market to reduce structural unemployment. First I am repealing all IR35 legislation, which was designed to prevent employers avoiding the cost of national insurance contributions on permanent staff, by the simple measure of charging the invoices of self-employed and agency staff to NICs also. Professional fees will be exempt. The increased revenues will be used to reduce employers NICs for all so that the measure is fiscally neutral.

In any case I am immediately reducing employers NICs to 12% and increasing the minimum wage and universal credits in line with the triple lock on the state pension. I am also introducing marginal relief for employers NI with a zero alowance of £1000 per week of payroll, and a lower band of £2000 at a rate of half the full rate.

Second my RH friend the Work and Pensions Secretary will be undertaking a full post-implementation review of the introduction of Universal Credits with a view to making it simpler and more streamlined and efficient. In particular he will ensure that the thresholds for and rates of clawback are also universal, and that once vetted claimants do not have to reapply every time they get a gap between jobs. This is particularly important for self-employed people who currently often decline short term or low paid assignments because of the hassle and delays in reapplying.

Within this context I am increasing the threshold, or earnings disregard, for clawback of universal credits to £50 per week. This will create a much greater incentive for unemployed people to make that first leap back into employment, and will also allow low paid workers in the taper to keep more of what they themselves have earned. This will both reduce the poverty trap and the pressure on food banks many of which are struggling to obtain sufficient supplies.

Mr. Speaker, I now turn to support for farmers and care homes. At first sight they do not have much in common but they are both essential to our wellbeing, are competitive within the private sector and yet need financial support if they are to produce both food and care at affordable levels and remain profitable. Furthermore farmers are in competition with foreign imports which are heavily subsidised.

For both industries I am introducing a public subsidy at 10% on turnover. This will be subject to a profit cap at 5% before tax to prevent profiteering by larger businesses at the expense of both taxpayer and customer. The subsidy is designed to promote sales, and the profit cap will encourage competitive pricing and support greater expenditure. Qualifying directors remuneration will be restricted. In future years the rate of subsidy will be adjusted so that no more than 5% of businesses liquidate each year.

Many businesses in a variety of industries receive public subsidies and there has been much concern at their profits. I am therefore extending the profit cap to all entities in receipt of public subsidy, though the cap may vary according to their capital investment requirements. I am also extending it proportionately to all companies with contracts with the public sector worth annually over 10% of their turnover.

Finally Mr. Speaker I come to the housing market. I shall be reducing house prices from now on by between 1 and 2% a year on average. This is easily done by giving the Bank of England that target and by tightening criteria such as mortgage to value and income to mortgage used by commercial lenders.

Now you may at first sight think that would make it more difficult for prospective purchasers to find and buy a new house, but in fact that is not so. For one thing the number of available houses out there does not change, and for another the supply is likely to increase because sellers will hurry to sell before prices reduce further. More importantly developers will no longer be able to make capital gains on their land banks and so can only build houses on them and sell them. In monetary terms the reduction in demand will be matched by a reduction is prices until all available houses are sold.

The misconstrued Help to Buy policy has just made matters worse, so I am in effect reversing it. Last year fewer new houses were built than before the policy was introduced over ten years ago and it has just pushed house prices even higher. Irrespective of whether we can balance supply and demand, the amount of credit tied up in the housing market means that house prices are likely to remain high. Yet house prices must come down if younger people are to buy when they get married and start a family and others to escape the parental nest and develop as independent adults.

Currently it takes on average over five years to build out a granted planning consent whereas no so long ago it was only two. It has been reported that there are hundreds of thousands of such consents gathering dust in the pending trays of property developers because they can make more money from capital gains. But it is important to understand also that they have themselves been squeezed by increasing land prices. As a result they have endeavoured to recoup their margins by resorting to dodgy practices such as denying buyers adequate snagging periods and tying them up into leaseholds with uncontrollable ground rent increases, and generally cutting costs and building to very low standards. Many such properties are now unsaleable. Mr. Speaker I am giving Help to Buy purchasers a new six month snagging period, with a survey at taxpayer’s expense to ensure objectivity, and with all restitution costs at the sellers expense.

My RH friend the Secretary of State for Housing, will be carrying out a full review of planning and related procedures including the possible repeal of the 1961 Land Compensation Act which gives 100% of all planning gain to landowners. We believe it may be more appropriate to divide planning gain equally between landowners, a national development corporation with powers of compulsory purchase to focus new development in the North where there are plentiful brownfield sites available, supported by regional policy which will encourage both people and jobs to move there, and local development corporations who can use the money for local infrastructure thereby creating balanced communities. The South East is overcrowded and current development priorities just make that worse. They are levelling down not levelling up. We will protect and maintain the green belt.

On social housing I am restoring the full housing benefit which will become affordable again as immigration falls. This will allow housing associations access to the City for development finance, and I shall be adding a government guarantee to help reduce borrowing costs.We will continue to support Right to Buy as it does not reduce total housing available but I am halving the discounts.

Following the Grenfell Tower Tragedy many leaseholders have become trapped with spiralling service charges which they cannot pay. I am therefore limiting service charge increases to inflation backdated to the date of the tragedy, and will refund landlords forced into loss by this, subject to reasonable limits on insurance premiums and other costs.

In summary Mr. Speaker I anticipate that for the coming year tax increases and expenditure savings with bring in around £80 billion and tax reductions and expenditure increases cost around £20 billion, giving my target net saving of £60 billion. I am also placing a five and ten year Source and Application of Funds Statement in the library and online. So now it just remains for me to I thank the House for their patience and attention during this speech. It is a budget for working people and small businesses combined with a strategy to save Britain, and I commend it to the House.

I have updated my annual graph below of our trade deficit with the EU and rest of the world. You may remember that last time it looked as though the deficit was narrowing. Was this some kind of Brexit dividend or just the effects of Covid? It was not clear.

But now look what’s happened. OMG! Wow! It’s as bad as ever! Quite clearly:-

1. The Tory TCA has FAILED, and

2. Those bastards in Brussels are still screwing us.

Look at the divergence which started in 2000, well before Brexit. How could that have come about? It can’t be us as we are common to both trends. It HAS to be Brussels. Deliberately, maliciously, persistently, albeit surrepticiously, they have been blocking our exports and our dozy officials in Whitehall haven’t even noticed or raised the alarm. I will leave you to guess their motives!

Now if we had a No Deal Brexit that sort of discrimination would be illegal under the WTO’s most favoured nation principle and we would be entitled to ‘countervailing measures’. But a bilateral trade agreement overrides that.

It’s time to give the EU a bloody nose by demanding countevailing measures and scrapping the TTCA. We are being played. Don’t fall for it.

Facing massive problems funding the budget deficit, record levels of structural unemployment, public sector wage claims, energy prices and national debt, a fragile bond market, an imminent recession and negative growth, the Chancellor, Jeremy Hunt, simply froze in the headlights.

A budget for growth it was not, given the forecast recession, but just possibly it might have eased that recession a fraction, so I am not going to carp over some pretty minor spending increases. It’s his strategy, or lack of it, I worry about.

Take the issue of childcare support for working mothers. He chooses to spend an additional £4bn on professional child carers. Leaving aside the age-old concerns about separating mothers from their new-born children, surely a much better and cheaper solution is Single Parent Circles. In this a social worker organises five single parents to form a group in which one looks after the children while the others go out to work and pay across a fifth of their earning to the first. Apart from the social worker it doesn’t cost the taxpayer a penny. You could even take it a step further and rehouse all five of them in a single large house where they will also get the mutual emotional support they need.

Obtusely Hunt has picked up on the problem of record unemployment (only about 10% of those of working age unemployed are benefit claimants), of which about 17% claim it is due to lack of affordable child care, but he has completely ignored the root cause of it all which is open borders. The points-based immigration system is supposed to exclude anyone who cannot earn a living in this country, but because Big Business prefers younger, cheaper, trained workers these are simply displacing older or untrained British workers and the result is the same. Only a switch to an auctioned quota system for total immigration will solve this. If we can reduce unemployment by 5% (8% to 3%) that in itself would save the Treasury over £100bn.

And just a point on immigration whilst I am on it. Total gross immigration is now around 75,000 a month. Of these ‘only’ around 5000 are illegals and refugees, and another 5000 could generously be attributed to people with rare skills and experience we cannot generate here. The rest, 65,000 of them, are simply cheap labour. They are undermining our economy, not benefitting it. Indeed, look at the GDP per capita growth rates over the past 22 years. They show a steady and persistent decline. No benefit whatsoever showing up as a result of massive immigration!

But back to the budget. No further relief for business from energy costs – that could cause havoc during a recession. But the main argument is over growth, with the Tories still stubbornly insisting that massive tax cuts are required to create economic growth. Wrong – it is investment that does that. Investment in productivity is uniquely being undermined in this country by three factors – the still ever-increasing trade deficit with the EU, open borders as above, and what I call ‘impotent’ investment, in other words the amount of available investment funding going into pushing up house prices rather than productivity. The Bank of England must be instructed to manage house price inflation separately from general inflation so as to squeeze available funding back towards industry. No need for tax cuts – and in any case there has been no shortage of funds in the City recently desperately searching for yield.

But what I found particularly amusing on Newsnight last night was Jacob Rees-Mogg pointing out that the Irish raise more in corporation tax (presumably % of GDP) than we do despite have a rate of only 12.5%, which he used to present a sort of Laffer-curve argument for cutting taxes. Presumably a logical extrapolation of this would lead to the conclusion that zero tax rates would result in infinite tax revenues? A reductio in absurdum, methinks!

But the real point Jacob has missed is that the Irish are taxing profits generated in the UK but booked in the Republic via transfer pricing. This is just another example of how the Bond Villains of Davos have their sticky mits in our till. Until we tax multinationals on the basis on their global profits apportioned by turnover they will continue to get away with it.

Rishi Sunak’s ‘solution’ to the small boats crisis is no such thing. He has no plan of where physically to put them! Rwanda could only take a few hundred and, while he recognises the need for other ‘safe places’ he cannot tell us where, how or when. He even thinks he can send them back to the EU, who are in fact absorbing even more than we are, by negotiating some sort of returns agreement. But why should they give us that? In return for what?

I have repeatedly advocated purchasing a substantial tract of habitable land somewhere OUTSIDE Europe, perhaps Central Asia, to be run in perpetuity as British Sovereign Territory. Yes they would want a high price for this but it would be a gold mine of foreign currency for them as well as an effective local regional policy. As the old saying goes, you cannot win a war on a budget. In any event as the colony develops it own economy the burden on the British taxpayer would reduce. The colony would have open borders so that they can self-segregate between genuine asylum seekers, who would stay, and economic migrants who would leave.

Interestingly I learnt over the weekend that recent polls in Sweden have shown that 79% who have been granted asylum do go home for holidays periodically. And in Germany it is 60%. Switzerland cancels their refugee status if they do.

Finally let us never forget that a far greater problem is legal immigration. Around 70,000 a month compared to ‘just’ 5000 illegals. A tiny minority, probably around 1000 a month, have skills we cannot source in this country, but the remainder are just cheap labour who are taking out more than they are putting in. We must scrap the points-based system which allows Big Business to bring in as many as they want, and substitute an auctioned quota system where the quota is set a fewer than the number who emigrate each previous year. Only then can we start to reverse the immense damage open borders have caused this country in so many ways.

This includes our environment. I am looking forward to David Attenborough’s new series on the British Isles. We have a record rate of extinctions going on. I wonder if he will acknowledge that open borders are the cause?!

We also have record amounts of crap in our rivers from overflowing sewage works. Yes that’s right. CRAP. Don’t let them tell you it is agricultural runoff. That has been going on for decades. There is nothing new about that. The fact of the matter is that immigrants crap. OK, so do we, and my political opponents through both ends, but our sewage facilities were previously adequate for purpose. Now they are not. So who’s going to pay for all that new investment. We are!

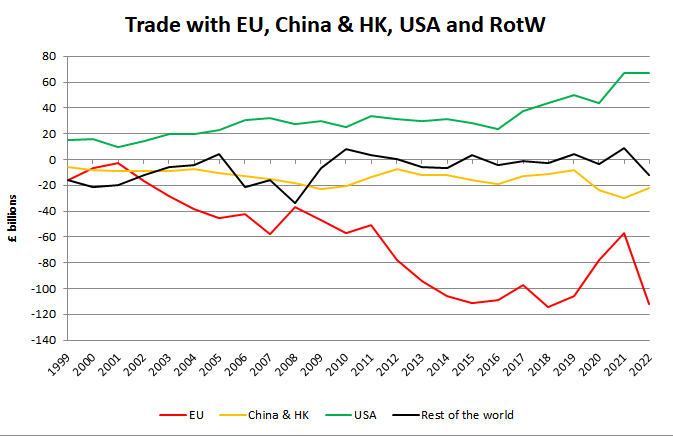

On 31st October the ONS published a breakdown by country of our balance of payments for 2021 so I have updated the graphs I do each year to show how our trade with the EU is developing.

We are now facing opinion polls showing a majority in favour of re-joining the European Union. How could this have happened?

Some Labour MPs, LibDems and Rejoiners think it is to do with labour shortages. They mistakenly associate tighter immigration with Brexit. But Brexit merely allows us to determine our own immigration policy, and that can be for more immigration if we so wish. So immigration now has nothing to do with Brexit. That shouldn’t be too difficult to get across but we have to make the point.

More seriously they associate Britain’s economic decline to Brexit. This is also nonsense as the above graphs illustrate.

The first graph shows our Balance of Payments (mostly trade) from the years 2000 to 2021, split between the EU (red line plummeting down through the floor) and the rest of the world (which I have split into three to show the US and China separately for comparison). Note that those other three lines taken together show a movement over that period into surplus. So at least until 2018 we have a divergence between the two areas – the EU and the Rest of the World.

How come? It can’t be us because we are common to both. It has to be Brussels. My theory (in the absence of any other explanation) is that since 2000 Brussels has be deliberately though surreptitiously blocking our exports in revenge for our not joining the Euro. The thieving bastards have been stealing our trade, and our dozy officials in Whitehall haven’t even noticed (or didn’t want to, which is even worse).

Is this important? Well yes it is because an increasing deficit presents British business with a contracting market, and business will not invest into a contracting market. No investment, no growth. It is the greater efficiency of production resulting from investment that creates economic growth. Tax cuts may help, but the opportunities to invest must be there in the first place.

This analysis is confirmed by the second graph which shows our growth rate plummeting alongside the EU trade deficit. The productivity gap is no mystery. It is a direct consequence of the increasing trade deficit with the EU, and explains why other countries are not experiencing it.

SO THE ONLY WAY WE CAN GET GROWTH GOING AGAIN IS BY RIPPING UP THE TORY DEAL AND USING TARIFFS TO OFFSET THE EU BARRIERS AND BRING THE BALANCE BACK INTO SURPLUS. ONLY UKIP IS SAYING THIS SO ONLY UKIP CAN GET THE ECONOMY GOING AGAIN.

Of course exporters will squeal if they have to face EU tariffs, but the uncomfortable fact for them is that our domestic market is far larger than our trade with the EU. Tariffs will reduce the volume of trade in each direction across the channel, but because we have a deficit the deficit will reduce as well. This means people in the UK will be buying more British stuff and less EU stuff. That presents British business with an expanding market to invest into thus generating investment and economic growth. So whilst those in exporting might struggle, those supplying the domestic market will have a bonanza – an import-substution led expansion.

Even better we can in fact protect our exports to the EU from tariffs, though not against the non-tariff barriers already there. This is because the new UK import tariff revenues will be much greater than the cost of the EU tariffs on our smaller volume of exports, so we can cross-fund them. It would be interesting in fact to start right now promising our EU customers a refund on any excess charges they are paying on British imports so we can confront Brussels with them. Doing so is entirely legal under WTO rules.

Looking at the past two years however we see that the deficit has reversed and it is tempting to say that is the Brexit Dividend! However It is much more likely to be due to Covid, but we will have to wait and see over the next couple of years. At least we can say it shows the current mess is NOT due to Brexit.

It is extremely unlikely that Lady Sarah Hussey meant any offence when she asked Ndozi Fulani where she came from at a Buckingham Palace reception last week. She was helping the Queen Consort entertain her guests; a role she has been playing for decades having been Lady in Waiting to the late Queen, and was simply taking an interest in her guest by way of conversation. It is perfectly normal to ask someone about their background in such situations. The late Queen did so constantly and indeed liked to be briefed in advance about whom she was going to meet.

If someone asks me where I come from I simply say Croydon. If I want to extend the conversation I say my mother was Welsh and father born and bred in Oxford. Still further back my ancestors were a mixture of immigrant Vikings, Normans and Saxons. To be able to say my parents came to this country from Barbados but that I was born here and am now a British citizen, as Fulani (born Mary Headley) could have done, would be much more interesting. Why couldn’t she have just said so nicely and politely? Ancestry is a very popular subject. The BBC has a whole series devoted to it. Nobody accuses them of racism.

Much has been made of how Lady Hussey pressed the point after an initial hostile reaction, but she would naturally have wanted to clarify the situation after being taken aback. Unfortunately it only made the situation worse, but how was she to know that? More likely Fulani was deliberately milking the situation as she appears to be making something of a career for herself insulting the Royal Family. According to returns to the Charities Commission her charity was set up in 2018 and has received £350,000 since then, but has not made any significant disbursements to anyone other than Ms. Fulani herself. The Palace should strengthen its due diligence procedures. Then she really would have been excluded!

Most of us do now know that black British citizens are peculiarly sensitive on this point. I myself have had the same experience and we learn that way. We are not mind-readers. I now avoid asking that question of black people, but that is my choice as a matter of individual moral sensitivity. Racism is defined in the dictionary as the belief that some races are inherently superior to others. Absolutely nothing in what Lady Hussey said indicated she ascribed to such a belief. Fulani simply misinterpreted the conversation – quite possibly deliberately.

We had the same situation arise in The Duchess of Sussex’s interview with Oprah Winfrey where she revealed that “questions had be asked about Archie’s skin colour”. Note, she did not say that “concerns had been raised …..”, which is what the media invariably reported. It is perfectly normal for prospective relatives to speculate about an unborn child’s characteristics and, for example, which parent they might more resemble. In the case of mixed-race parents skin colour is an obvious interest.

It is highly regrettable now that the Palace has caved in to the criticism and thrown Lady Hussey to the wolves. If anything Ms. Fulani owes Lady Hussey an abject apology for the distress she has caused. The late Queen would am I sure have shown much more backbone. She might have issued a statement along the following lines:

“It is with deep regret that we have learned of a substantial misunderstanding last week between a member of the royal household and a black guest at a reception here at Buckingham Palace. The guest is claiming she had been subjected to racist questioning. Opinions on this may vary but may I take the opportunity to reassure our black community that no offence was intended and that we value highly the involvement of black people in British life today.

Misunderstandings are commonplace in life, particularly where people of different backgrounds come together. Let us all learn from such experiences and always try to understand the other person’s point of view. I am sure we can overcome such differences and see the good in others, as well as the shortcomings in ourselves, and that way develop peace and understanding amongst us all.”

You don’t want to get too tied down by the General Theory. It’s complexity undermines its validity and he appears to have been transfixed by Einstein’s general theory of Relativity which genuinely did extend the boundaries of physics rendering what we now call Classical Physics as merely a special case. Go to the extremes of matter moving close to the speed of light or the interaction of sub-atomic particles (or waves – see Heisenberg’s Uncertainty Principle) and the classical laws of physics break down. But that does not mean that classical physics is redundant. It is still used for every day understanding and technology including rocket science! I suspect that Keynes wanted to be seen as having done something similar for economics, but he didn’t.

However he did undoubtedly extend our understanding of fiscal macroeconomics beyond the received wisdom of Alfred Marshall and the Cambridge school, which were largely based on microeconomics, and those theories are as valid today as they were then.

There are three broad elements to macroeconomics: fiscal, monetary and international trade. The first two are now broadly understood, but I see little evidence of any understanding of the economics of international trade amongst our politicians and bureaucrats. Free trade is commonly regarded as a general panacea but in fact it breaks down in the case of substantial deficits. A good example of this is the EU Single Market. That is free trade, yet the UK’s experience of being in the single market has been a disaster, resulting in a trade deficit now of nearly 7% GDP, which undermines investment and growth. Clearly business will not invest into a contracting market, and UK GDP/capita growth has plummeted in parallel.

This is a question recently posed on Quora where I frequently post. Here is my answer.

Depends how it is funded. If that is by corresponding cuts in government expenditure then the net effect will be zero. However if it is by increasing borrowing then net demand in the economy is increased. That is what we have seen since the banking crisis and to combat the ever-increasing trade deficit with the EU over the past twenty years which has destroyed jobs. The result is record levels of both national and personal debt. Indeed they have over-done it which is one of several reasons why we now have a shortage of labour.

It is worth noting at this point that increasing demand in the economy to reduce unemployment, sometimes referred to as Keynesian economics after the way the famous economist John Maynard Keynes advocated ending the depression of the 1930’s, is not at all the same thing as economic growth in our standard of living (GDP per capita). “Treasury Orthodoxy”, now being blamed by the Tory leadership candidates for the lack of growth, is to balance the books over the course of the economic cycle, not year by year. That allows for borrowing during a recession to reduce unemployment provided it is paid back during a boom so that debt as a percentage of GDP remains constant or falling. Whilst it has nothing directly to do with growth it does lead to a disposition in favour of inflation to reduce the debt rather than balancing the books with tax increases or expenditure reductions. Inflation reduces real interest rates and hence savings and investment thereby undermining growth.

Internationally there is much evidence to suggest that smaller government produces higher rates of economic growth, the logic being that high levels of government expenditure uses up finance available for investment and therefore ‘crowds out’ the private sector which produces most of that growth because it is subject to competition. In the UK however the electorate demands expensive public services (eg the NHS) and a reliable welfare state making that difficult to achieve. That means separate policies are required to make public services much more efficient (the potential is huge, not least from introducing some proper accountable top management for each service) as well as finding other sources of finance, such as a Sovereign Wealth Fund or optional means-tested access to the private sector for services, if we are to reduce tax levels permanently. This is the essence of a centrist, radical economic strategy.

Over the past twenty years we have seen very little growth in our standard of living, This “productivity gap” is in fact a direct result of our increasing trade deficit with the EU, which presents British business with a contracting market and thereby little incentive to invest, and of open borders causing increasing levels of structural unemployment (the mismatch between people and jobs by skills and location. Square pegs will not go into round holes). Interestingly record levels of immigration have not provided any boost to growth. Only a quota system for legal immigration will solve that. The points-based system, which Tony Blair introduced in 2006, is too easily gerrymandered in favour of Big Business, thereby creating a self-perpetuating immigration spiral. Unless business is forced to train up British workers by a quota system the levels of structural unemployment will just get higher. A Tory government will never do this as their donors in business will not allow it.

The main condition for growth is investment by British business which carries more efficient means of production (productivity). For that you need both an expanding market and available additional labour resources. If you try to increase demand when there is a shortage of labour the result will be a combination of increased inflation, immigration and imports, the last giving all the investment benefit to foreign business. Open borders also imports wage compression which offsets the inflation and so masks the alarm bells at the Bank of England, which uses inflation as an indicator of an over-heated economy and the need to increase interest rates to control it. Hence the immigration spiral.

Many of us remember the Boom and Bust at the end of the 1980’s when Nigel Lawson’s 1987 budget cut income taxes substantially just when the economy was expanding as a result of Geoffrey Howe’s earlier cuts in credit controls. The result was that people used the extra money in their pockets to jack up their mortgages and chase up house prices.

The only way now to present British business with a sustainable expanding market is to reduce and eventually eliminate that trade deficit with the EU. This has grown steadily over the past 22 years to over 6% GDP while our trade with the rest of the world has moved from deficit to a steady 1% surplus. This divergence demonstrates clearly how the EU acts surreptitiously and maliciously to block our exports, (probably in revenge for us not joining the Euro), and the Tory deal has just allowed them to keep on doing that. Only a full No Deal Brexit will give us legal protection from such practices under the WTO’s ‘most favoured nation’ principle which applies where no bilateral trade agreement is in place. Furthermore it would enable us to use tariffs to offset the EU non-tariff barriers and take back control of our economic sovereignty as well as our legal sovereignty. Free trade on top of a deficit only increases that deficit and makes matters worse – simple mathematics!

Furthermore recovering £120 billion of trade deficit improves total GDP by that amount which in turn improves the tax base which produces about one-third of GDP as tax revenues. That means an extra £40 billion of tax revenues without increasing tax rates one iota.

It is interesting that neither of the Tory leadership candidates has drawn a distinction between the cost-push inflation that is now being imported on oil and gas wholesale prices, and over which no amount of increased interest rates will have any effect at all, and the monetary inflation resulting from government mismanagement and over-heating of the internal economy. We have to address both types separately with separate policies.

Cutting direct fuel and energy taxes makes a lot of sense to offset the imported inflation and keep domestic fuel and energy prices stable, thereby cutting off a wage/price spiral at the knees. Means-testing energy bills will also reduce the cost of this and ensure the poorest get the most help, at least pro-tem until the danger has passed. This will probably prevent most of the forecast recession. This can be done by enabling householders to direct their energy suppliers to send their bills direct to the taxman, who will pay them. The taxmen then applies the means-test to the increase since the start of the Ukraine War and recharges the householder through their PAYE code or deduction from benefits. Similarly for business, the taxman can agree to pay a percentage of the increase in return for a profit cap. For example if 100% of the increase is accepted the profit cap would be 1%, whereas for 25% it could be 4%, or some such gradient.

There has been the usual nonsense from Labour about imposing price caps, but this would inevitably lead to blackouts and supply shortages. There has also been talk of windfall taxes on suppliers without any consideration of what level of profits is normal and necessary for investment. Energy company profits comprise a significant parts of most pension fund portfolios. However a profit cap set at say 5% before tax does make sense as a general policy which should also include wind and solar farms.

Then we all the nonsense about converting to electric cars. These are now actually more expensive to run than petrol cars! Not only that, but the electricity that comes out of your socket is hybrid! If it is generated that way, as it is because of the proportion that comes from gas, then what comes out will be hybrid as there is no way of separating them in the grid. Indeed many of the blackouts now predicted for this winter will be due to electric cars. It would take massive investment to expand the National Grid to cope with everyone plugging in their electric cars at the same time, and supplying electricity in this way involves substantial transmission losses. Far better to go for hydrogen-hybrid and carry your fuel around with you just like petrol.

However in parallel with all this the Bank of England must get its act together on interest rates to get some flexibility back into the labour market. I should also like to see them given a quite separate target to stabilize house prices using credit controls, as house price inflation often leads general inflation. The former will be difficult as there are a number of other factors which have glued up the labour market. Incredibly we now have a record 8% of the working-age population who are classified as economically inactive. Whilst much of this is the result of many years of open borders, it is also due to the botched implementation of Universal Credits, IR35, the traditional poverty trap as well as hangover from the Covid restrictions.

Perhaps the silver lining is that 10% inflation on top of a £2 trillion national debt releases an extra £200 billion for government expenditure if the aim is to keep the debt at a constant percentage of GDP in line with treasury orthodoxy. My suggestion would be to save half and spend half, and allocate half the spending to tax cuts and half to budget increases. That should be sufficient to knee-cap energy prices and provide some protection from inflation for public-sector workers and those in need as well as fund essential public services acceptably.